Andre's Next Frontier: The Keep3r Network Overhaul

Helping you make sense of Andre's tweets.

The story so far.

Keeper Network was launched by Andre in October 2020, with a blase medium article and subtweet that still attracted speculative frenzy amongst the DeFi community. Keeper V1 was a platform for protocol developers to efficiently outsource and decentralize development operations tasks known as jobs. Protocols have to rely on jobs to work correctly because smart contracts cannot automatically execute a function by themselves. Every action must be triggered by a transaction call from an EOA. EOAs perform these actions in a manner as required by the protocol, and are known as keepers.

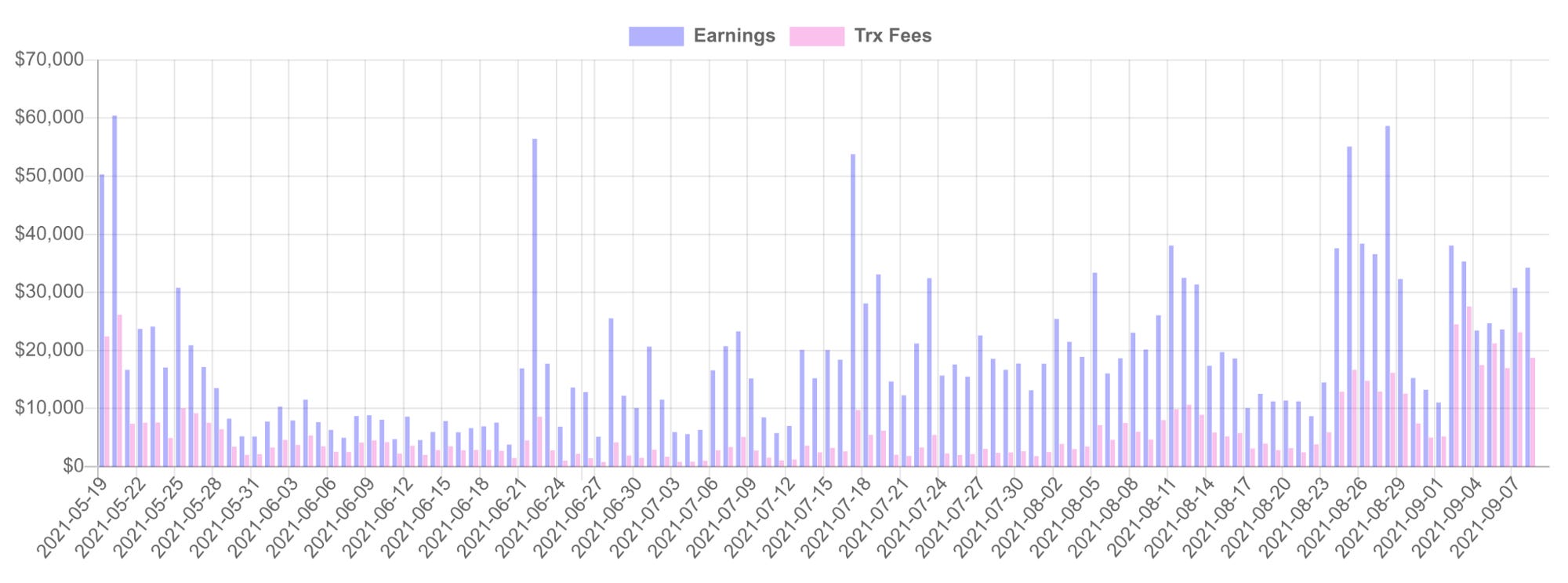

The need for Keepers to service dAPPs is huge, but there is a limit to the sophistication of the tasks involved (in the current dapp landscape), thus capping keeper earnings. Aggregators need keepers to call harvest() at regular intervals. Debt protocols need keepers for timely liquidations. Nevertheless, most protocols still prefer to run their own keepers or, like what Liquity does, embed incentives to reward keepers within their own set of smart contracts. Protocol earnings accruing to KP3R Keepers have only marginally increased in the past few months, fluctuating within the 15K-30K USD range.

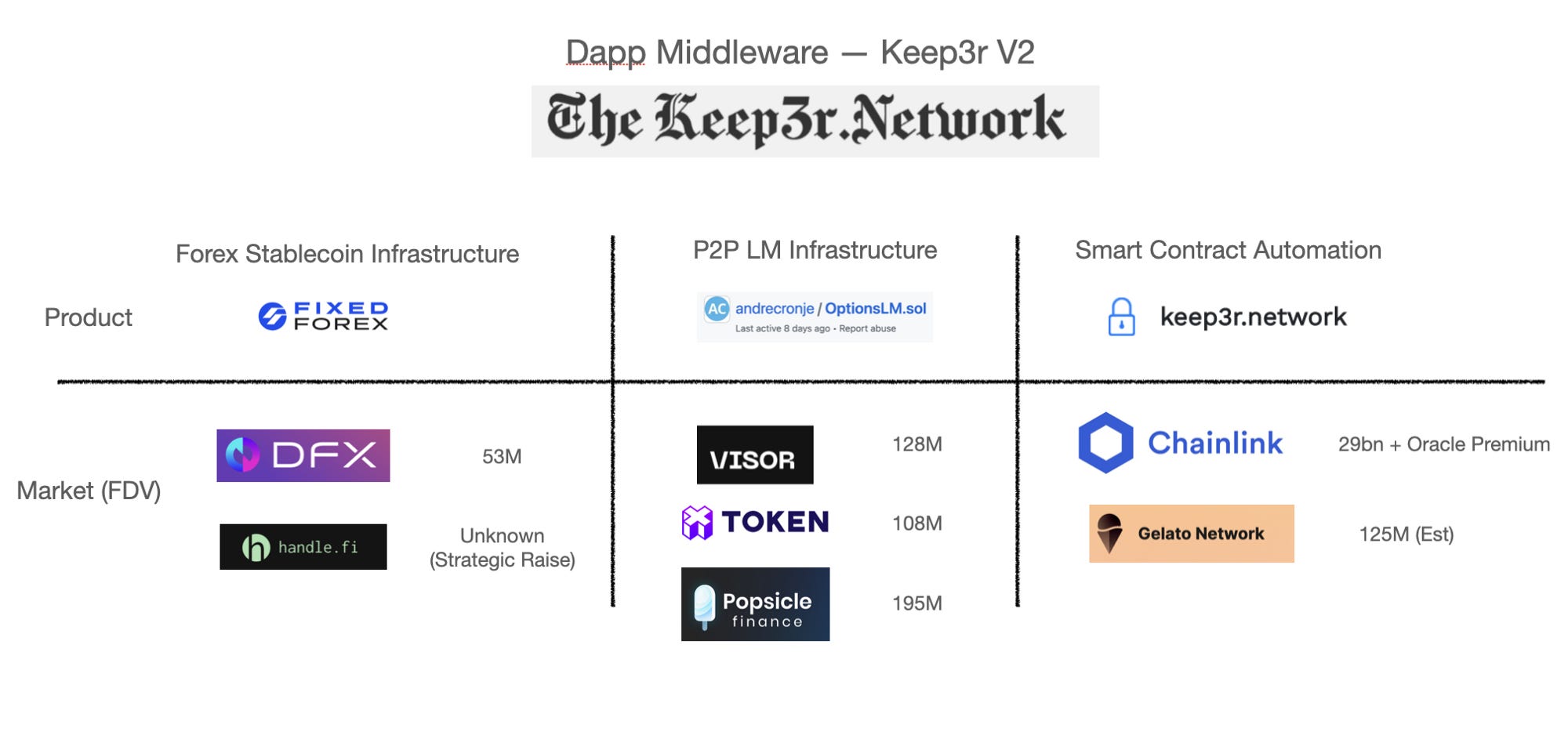

Expansion to Keeper V2

A few weeks back, in a similar pattern of abruptness, Andre revealed that he intended to incorporate multiple products into the Keeper Ecosystem. The Keeper V2 family now extends to 4 new products:

Fixed Forex, a protocol for permissionless minting of forex stablecoins with gentle liquidations

A protocol for dAPPs to launch liquidity mining programs with token options as rewards, unnamed. rKP3R is an initial experiment with this.

A protocol for automated and fungible liquidity provision on Uniswap V3, unnamed. (This appears to be used natively for KP3R liquidity only)

DeFi Wonderland, a pseudo accelerator platform.

In general, with all these primitives in place, Keeper Network should now be thought of as an out of the box protocol services platform for dapps. Protocols can also utilize Keeper Network’s inbuilt oracle systems, which is synergistic with keeper automation.

The KP3R token

Keep3r tokenomics are thus in for a massive overhaul. Notable changes include:

A curve-like Vesting mechanism that reduces sell pressure

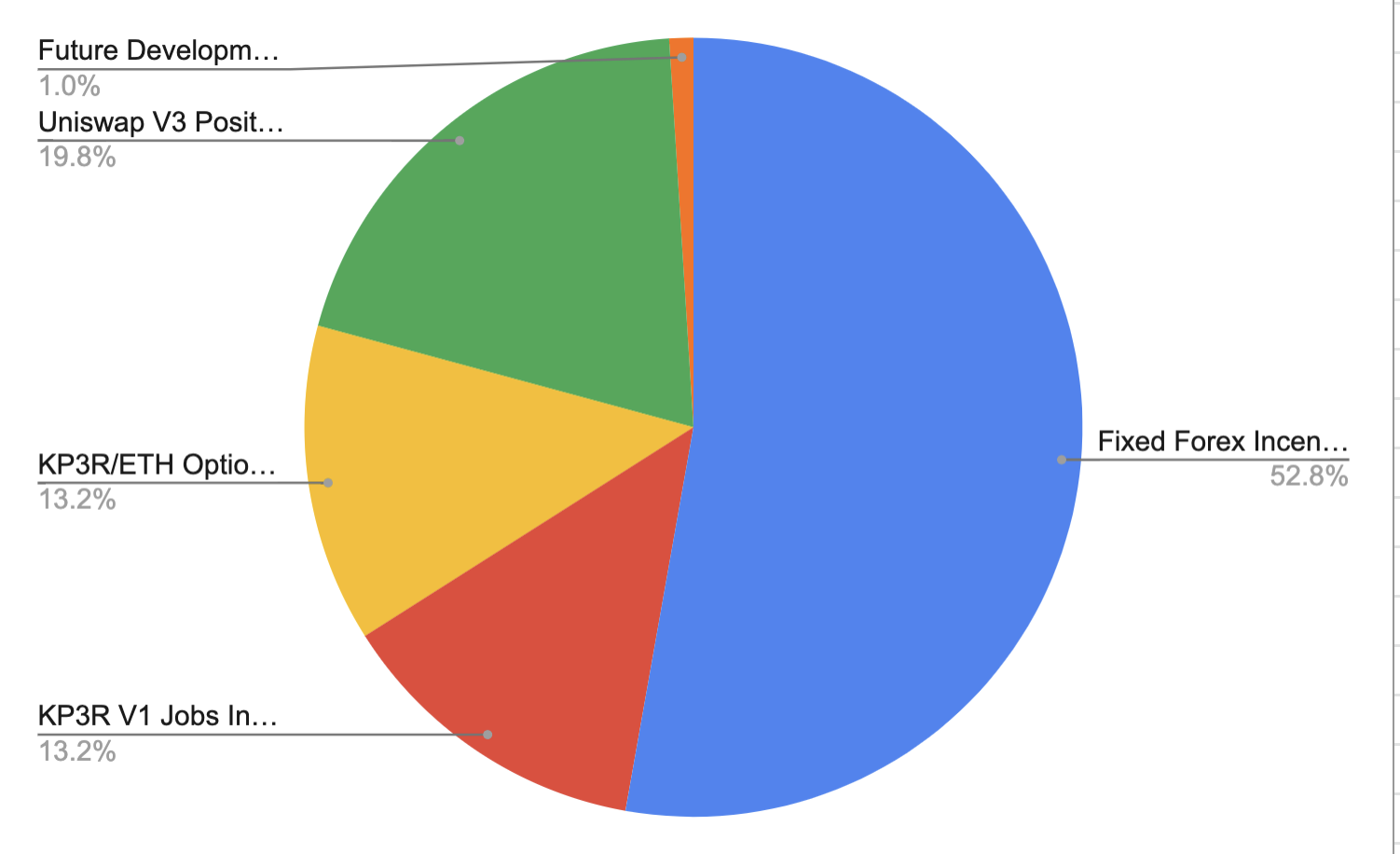

Revenue from all 4 products being directed back to vKP3R holders

Unfortunately, Andre has been rather vague regarding the future tokenomics of KP3R. We do know, however, that there will be a maximum cap of 7.5K KP3R incentives issued (~3 mil USD/week), which is high compared to even Avalanche’s liquidity mining programmes (7.5mil/3 months for Sushiswap). These incentives are already in place for the fixed forex protocol, emitted in the form of rKP3R. We can assume that other rewards should be emitted in rKP3R as well, which limits sell pressure.

rKP3R is basically a call option for KP3R, which Andre put in place to prevent huge downward pressure in KP3R prices from farmers who dump. The strike price for rKP3R is 24 hr TWAP-50%. Farmers can profit off the difference between the option strike price and actual KP3R price.

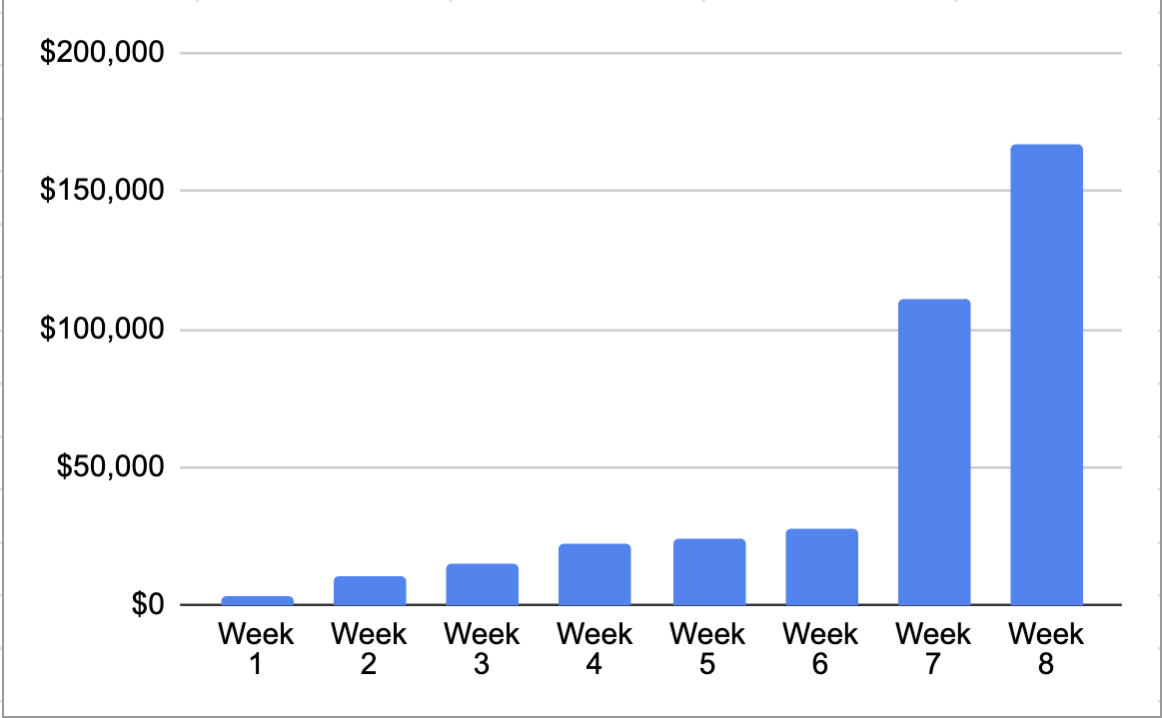

vKP3R will earn fees on all of its products, but the Fixed Forex protocol which is already live on mainnet is now its key revenue driver. Taking a 7d interval, KP3R currently trades at a ~126x Price/Earnings (Monthly) ratio, not far off from other debt-based protocols like Compound (105x) and Aave (97x). We’d expect this ratio to further drop favourably as other revenue sources take over, and Fixed Forex TVL will continue to boom, due to CRV gauge incentives.

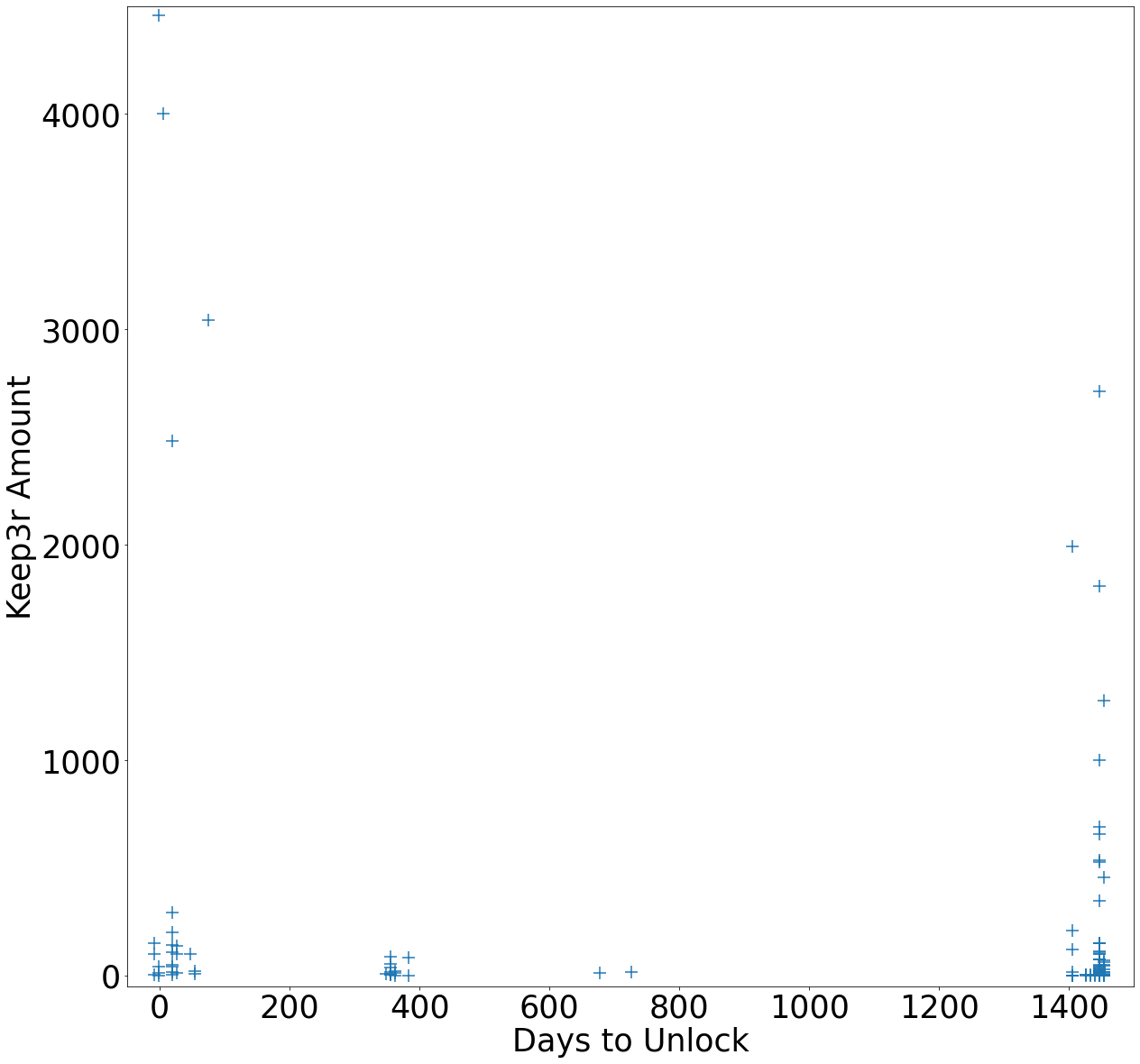

Vesting Data

Keeper Network’s official claim that the average vesting period is more than 3 years is indeed true. These are lower numbers than Curve (3.7Y mean) but higher than FXS (1.26Y mean). We can also plot a more accurate picture of the vesting distribution using on-chain event logs. The weighted average vesting period is currently 1.9 years.

As of today, 12% of KP3R is vested and 24% is supplied on exchanges. This proportion is lower than other protocols with vesting mechanisms: 74% of CRV is locked, while 22.1% of FXS is locked. Moving forward, we might expect the vesting mechanism to continue placing upward pressure on prices in the next two weeks.

Assessment and Future Trends

The DeFi market is maturing to pursue optimization (capital efficiency, risk management) while maintaining “laziness”. The potential of smart contract automation via bots is yet to be realized. It will not be unwise to bet on more protocol-as-a-service features being built on existing dAPPs. Some examples that have surfaced recently: Automated Health Factor Maintenance from Aave, limit orders on Spookyswap.

While Andre presents considerable clout and influence, his most successful protocols win on high technical competency and a cult-like developer community. Such advantages are trivial in a protocol-to-protocol sector which places premiums on ease of integration, customer support, and branding. Gelato Network remains dominant in this regard.

I believe increasing demand for non-USD stablecoins as a hedge against cryptocurrency volatility is Keeper Network’s strongest value hypothesis. Fixed Forex features much lower Loan-To-Value (LTV) ratios and more flexibility in collateral type than its counterparts. With more investors hedging against USD depreciation, I expect strong growth in protocol revenue from the Fixed Forex arm.

P.S: Is there demand for Forex in DeFi?

This is a question I’ve been thinking a lot about. The market capitalization of EUR based stablecoins both centralized (Statis Euro, EURTether) and decentralized (sEUR) have been stagnant/decreasing these past few months. The APYs on forex pairs on Curve regularly exceed USD pairs, so there clearly isn’t much demand from DeFi users to farm with them.

The traditional forex market is huge, with around 2+ trillion USD spot volume done daily. But my thinking is that this is usually derived from 1. Traders speculating on currencies 2. Firms hedging currency risk, and 3. Peer to peer remittances. 2 and 3 are not really applicable in DeFi, since having multiple currencies is a bug, not a feature, of our current financial system. I’m not so sure about 1. — is there much to speculate on if 2 and 3 don’t apply to DeFi markets? And why speculate with DeFi then? Forex isn’t very gated. Tokenized forex derivatives may be useful but we haven’t seen such instruments being used yet.

I also don’t think an internet-native industry where most money circulates internally (instead of being withdrawn out) will need to further fragment liquidity by introducing new forex pairs against other assets.

USD may be displaced by another currency, or even by a non-fiat-pegged stablecoin, as the single dominant medium of exchange in crypto in the next decade, but the case for forex trading across different currencies in DeFi is not strong.